20:16

20:16

Unknown

Unknown

European, Chinese Economic Data May Underscore Divergence From US, Could Weigh On Gold |

(Kitco News) - Next week brings more attention to eurozone and Chinese economic data, and the results may serve to underscore the monetary policy divergence between the U.S. and the rest of the world.

That could result in the U.S. dollar gaining further and putting pressure on gold, which could reverse some of the gains the yellow metal enjoyed Friday.

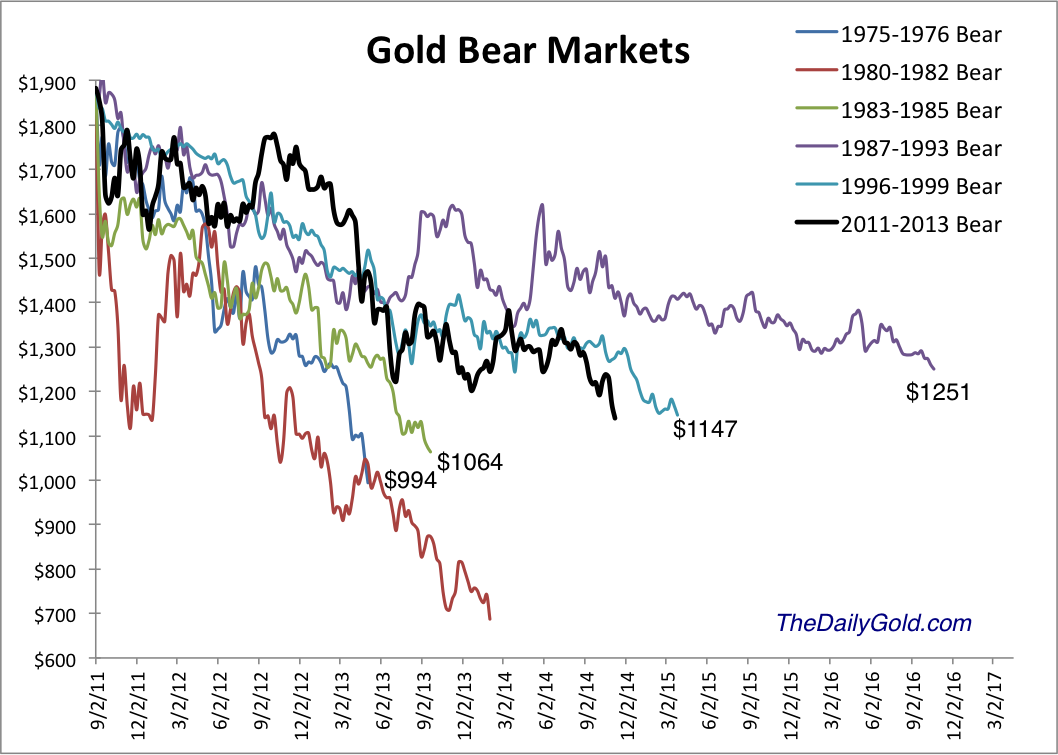

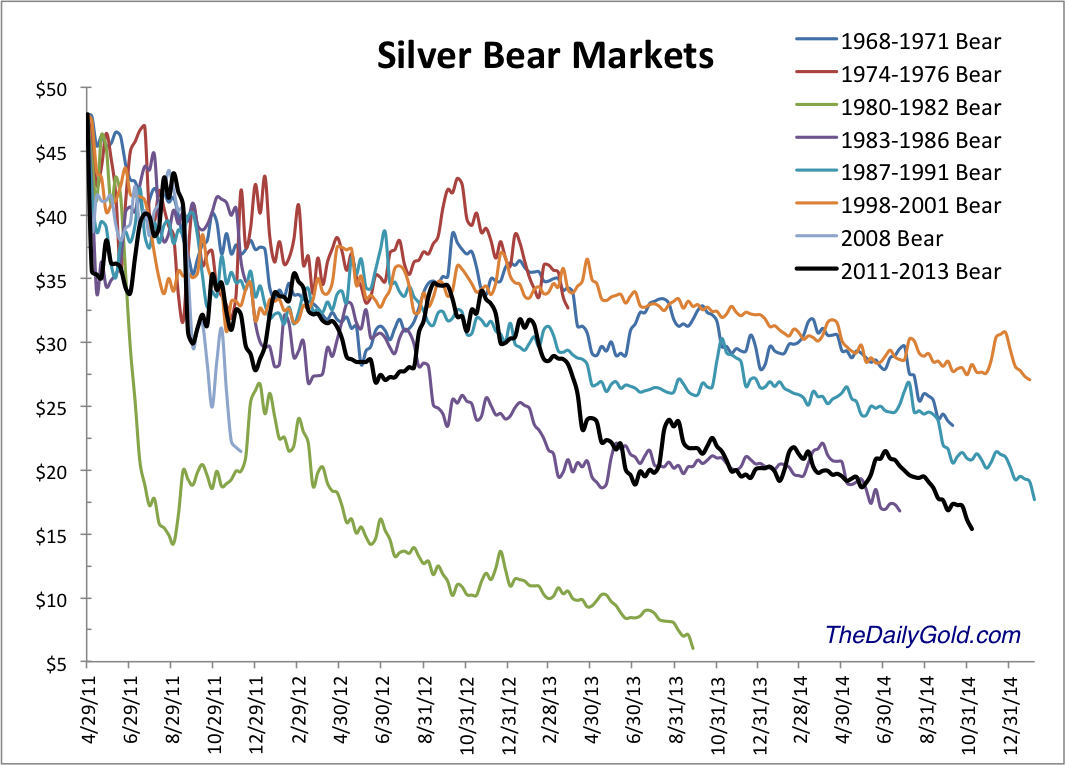

December gold futures rose Friday, settling at $1,169.80 an ounce on the Comex division of the New York Mercantile Exchange, down 0.09% on the week. December silver rose Friday, settling at $15.714 an ounce, down 2.28% on the week.

Participants in the Kitco News Gold survey remain bearish. Out of 36 participants, 23 responded this week. Of those, six see higher prices, 14 see lower prices and three see prices trading sideways or are neutral.

Gold prices rallied off the four-and-one-half-year lows set overnight Friday around $1,130. Analysts said the combination of short covering after the U.S. nonfarm payrolls report, a weaker U.S. dollar and news of stepped-up military action in Ukraine pushed gold above technical-chart resistance around $1,160.

The U.S. Labor Department said Friday the U.S. economy created 214,000 jobs in October, with the unemployment rate lowered by 0.1 basis point to 5.8%. That figure was under the 230,000 jobs expected. Employment gains for September and August were revised up by a combined 31,000.

“Overall it was an OK jobs report. I don’t think it changes overall our positive outlook for the U.S. economy,” said Rob Haworth senior investment strategist, U.S. Bank Wealth Management.

What it does is give the Federal Reserve some room before it needs to raise interest rates, particularly since wage growth remains low, he said. “At this point the chance of a rate hike in March is low,” Haworth said.

The economic calendar in the U.S. will be light next week, so traders’ focus will be on data expected out of Europe and Asia, analysts said. And the reports will likely to reinforce the sluggishness seen in Europe and China.

Robin Bhar, head of metals research at Societe Generale, said if the economic data from Europe and China come in weak, they will underscore the prevailing view of the differences between the U.S. and those regions and support the dollar.

In Europe, several countries will release their first third-quarter gross domestic product data, and China will release reports on industrial production growth, producer price index and export data.

“The data in the U.S., including the jobs report, and (European Central Bank President Mario) Draghi being very dovish (on monetary policy) means the dollar continues to be bid up. That’s going to keep the pressure on gold,” Bhar said.

“Next week there will be more views on policy divergence with the Fed (Federal Reserve) needing to eventually tighten rates, and Japan, the eurozone and even China showing their economies are growing much slower and (they) need easy monetary policies,” he said.

Haworth agreed.

“Policy divergence is well entrenched at this point,” he said. “I’ll be most interested in China’s data. We’re focused on what is the real tenor of growth in China at this point. We expect it to not be 7.5% or 8% as it has been in past, but will it be under 7%? That has some ramification on big trading economies like Europe,” he said.

Related Stories:

- Passage Of Swiss Referendum Would Support Gold, But Other Central Bank Actions Could Offset It –TDS

- IBA Named Third-Party Administrator For LBMA Gold Price Mechanism

- Financial Markets Need Stronger Security Against Cyber Attacks – CFTC's Massad

Gold put in a solid rally on Friday, pushing through some initial technical-chart resistance points around $1,160. However, several gold-market watchers said the gains may be more of a selling opportunity than the start of a further move higher.

“I can’t get too excited about it. The best thing you can say is it produced an outside day up,” said Charlie Nedoss, senior market strategist at LaSalle Futures Group.

An outside day on a technical chart occurs when the current day’s prices exceed the high and the low of the previous day.

Nedoss said because gold prices fell so far, so fast, they remain under major moving averages. He said the 10-day moving average sits around $1,184.

“Until we get above there, I think people will use the rally as an opportunity to sell. The dollar is so strong, especially compared to the rest of the world,” Nedoss said.

Haworth said traders who were short gold this week likely sought to book profits. He also does not expect Friday’s gains will hold in the medium term.

“For us, as we look over the next couple of months, the dollar trend is still stronger, the U.S. economic trend is positive, the Fed ended QE (quantitative easing) and may raise rates, and geopolitical risk is not a major factor going into the year end. We’re not looking for any support until gold gets under $1,100,” he said.